On December 3, 2024, Yoon Suk Yeol, president of South Korea, declared martial law claiming a “legislative dictatorship” was fighting against him. To make it even more dramatic, he did so live on television.

Many everyday people in the West probably forgot this ever happened, if they knew at all. After all, a lot has happened since then. But this was nearly unprecedented political turmoil in the world’s 14th-largest economy.

The National Assembly, which is akin to the U.S. Congress, was stunned. Military and police forces tried to stop legislators, but they were eventually able to enter the building and vote to lift martial law. Not only was Yoon impeached, but he is now on trial with the death penalty on the table.

And as unbelievable as that was, South Korea’s troubles were only just getting started.

A few months later, Donald Trump announced a new barrage of tariffs. South Korea is heavily reliant on exports, which make up half the economy. The country exported a record $127.8 billion to the U.S. in 2024, a 10.5% increase compared to 2023. That’s one-fifth of all South Korean exports.

As the world’s 14th-largest economy, South Korea is home to industrial and technology giants like Samsung Electronics (SSNLF) and Hyundai Motor (HYMTF). And most of their products are sold overseas. China is their biggest trading partner, but the U.S. is close behind. This was about as bad as it gets.

The new tariff system is a reality check for many countries, but it was a huge blow to South Korea. Many of its companies, including Samsung and Hyundai, are aggressively expanding manufacturing in the U.S. to avoid tariffs (with some success). But it’s still painful, and short-term profits will be impacted.

Now, given all this, you might expect the South Korean stock market to look like a plane crash. You’d probably even bet on it.

So, how’s the country’s equities market holding up?

{kind=link}

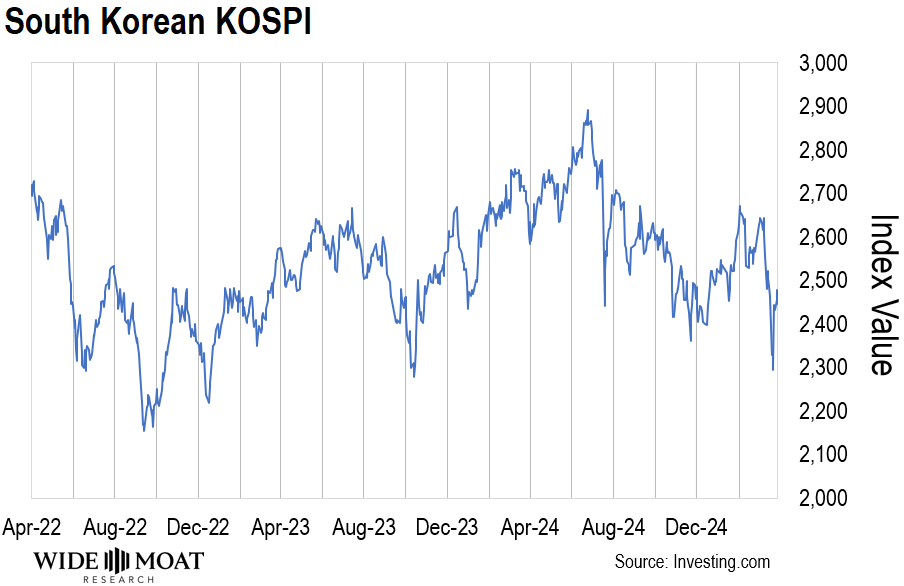

This is a three-year chart of the South Korean stock market (KOSPI). Can you see when martial law was declared? What about the U.S. tariffs?

When the South Korean president made his famous television speech, the market closed at 2,464. At writing, after the serious political drama and U.S. tariffs that South Korea is especially vulnerable to, it’s at 2,477.

How is that possible?

In 2023, the 247 publicly traded South Korean companies earned $226 billion. Total profits for listed companies in 2024 are estimated to be… $350 billion.

That is remarkable, but what about going forward? The Bank of Korea revised down its 2025 GDP forecast to 1.4% if there is a full-blown trade war with the U.S. Otherwise, it’ll be higher.

But that worst-case scenario is already dead on arrival. The U.S. administration exempted a long list of technology products made in South Korea that rely on Chinese imports including laptops, processors, and chip-making equipment. They’ve even announced potential short-term tariff exemptions with Hyundai and Kia.

From an outsider’s perspective, it looks like the Trump administration is more interested in manufacturing investments in the U.S. than tariff revenue. And South Korea is playing ball.

So, what am I trying to say?

Fundamentals, Not Headlines, Drive Markets

Investors are nervous right now, understandably so.

As a result, we’re seeing several knee-jerk rallies and crashes on each new headline. Perhaps you’ve fallen victim to that thinking in recent weeks. But if you take nothing else away, know this – fundamentals, not headlines, drive markets.

The headlines you read every day get us to think emotionally, not logically. And politicians are even better at this than the media, and that’s saying something.

Don’t fall victim to that trap. And here’s why.

{kind=link}

Here’s a three-year chart of the S&P 500. At the very bottom of the recent sell-off, 11 months of gains were lost. Since the rebound from the bottom, it’s only nine months. Over the past three years, however, the market has gone up 35%.

Let’s compare that to the Great Recession of 2008/2009. The S&P 500 lost more than half of its value with a low of 677. About 12 years of gains were erased at the bottom. At writing, the index is around 5,500. I know, it seems almost unbelievable. That’s because no one talks about steady market gains, only the rare declines.

The point I’m making is that there is always something to be worried about. There’s always some crisis, some calamity, some new headline to make you afraid. For decades, stocks have climbed wall after wall of worry.

As an investor, that’s not where our focus should be. Ten years ago, earnings per share for the S&P 500 were $116.73. Last year, the number was $210.17. That earnings growth happened through the pandemic, democratic and republican presidencies, and plenty of mayhem to distract us.

But in the end, none of it mattered. Not here, not in South Korea, and not anywhere else where businesses are free to adapt to changing environments.

Headlines and temporary crises cause temporary pain for many investors. But, again, headlines don’t move markets in the long term. Fundamentals do.

If you’re a long-term investor, stay the course and follow the advice my colleague Nick Ward gave last week – just do nothing.

And if you’re the type of investor that wants to take advantage of this volatility, you have options…

My longtime readers know one of my favorite strategies is to sell put options on select high-quality companies. It’s a simple strategy.

We either collect an instant yield on cost in the form of option premiums. Or, in the event we’re put shares, we own some of the best companies in the world at or near 52-week lows.

Heads we win. Tails we don’t lose.

For our latest trade, we zeroed in on Blackstone (BX), the world’s largest private equity firm by assets under management. We secured a 10.6% instant yield. And since the trade takes place over 72 days, that comes out to 66.5% annualized. And in the event we’re put shares of BX, our effective entry will be below the 52-week lows. That would be an incredible entry for a business as sturdy as Blackstone.

So, once again, read the headlines, but don’t trade off them. Stay the course, keep the faith, and look for opportunities to take advantage of market dislocations. And odds are we’ll have plenty of those opportunities in the near future.

Regards,

Stephen Hester

Chief Analyst, Wide Moat Research