If you were going to make a Mt. Rushmore of investors, who would be on it?

Warren Buffett, maybe?

Buffett officially retired at the end of last year. He ran Berkshire Hathaway (BRK) for 60 years. During that time, the value of BRK shares rose by 6,099,294%. That would be about 19.7% annualized. We can compare that with the 10.5% from the S&P 500 over the same period.

Maybe you’d also include Buffett’s wry old partner, Charlie Munger, as well. Or, maybe Buffett’s mentor, the father of modern value investing, Benjamin Graham.

I don’t think anyone would object to those inclusions.

Maybe Peter Lynch, known for his amazing success at the Magellan Fund (29.2% annualized returns over a 13-year period), deserves a spot. What about James Simmons, who produced the highest ever returns in the hedge fund industry, compounding his data-driven Medallion Fund at a 66% annualized rate from 1988 to 2018.

No one’s going to argue with any of these picks either.

But for my personal Mt. Rushmore of investing, I’d say Ronald Reed deserves a spot.

You’ve probably never heard of him, but he has a lot to teach us…

America’s Secret Millionaires

Ronald Reed is one of my favorite stories.

Reed grew up impoverished. He was the first personin his family to graduate high school. And after graduation, he entered into the U.S. armed forces, serving in World War II. After his military service, Reed worked as a gas station attendant and a janitor at JCPenney.

He didn’t wear expensive clothes. He didn’t drive a flashy car. Throughout his life in Brattleboro, Vermont, he was mistaken for someone down on his luck. People would offer to buy him coffee or pick up the tab for a meal. But Ronald Reed was a multimillionaire.

Reed lived below his means for decades. He took those blue-collar savings and invested them into well-known dividend growth stocks such as Johnson & Johnson (JNJ), General Electric (GE), and JPMorgan Chase (JPM).

After his death, Reed made headlines when news broke that he had bequeathed over $1 million to his local library and nearly $5 million to the Brattleboro Hospital.

I love stories like Reed’s. It shows that buying wonderful companies, holding them, and reinvesting the dividends can work for anyone who’s patient and disciplined enough to adhere to the long-term strategy.

They also show that anyone can make a big difference in the world and leave a legacy.

That’s my goal. I’m not stashing cash away in investment accounts just so I can see how big the numbers get. Sure, I want to create financial security for my family. But I also think that being a good steward of wealth involves being generous to the less fortunate and helping needy causes.

The problem is, generating significant wealth takes time. Reed worked for more than 50 years and let his wealth compound for another couple of decades in retirement. Building sizable wealth takes time. But there is a way to give that journey a boost in the right direction.

Using Closed-End Funds to Bolster Passive Income

Today, I’d like to talk a bit about how closed-end funds (“CEFs”) might be your answer.

CEFs are publicly traded investment vehicles that raise capital with an IPO and then provide investors with exposure to (typically) actively managed investment portfolios. Unlike exchange-traded funds (“ETFs”), which see their share counts rise and fall due to investor demand, CEFs don’t make new shares available post-IPO. That’s what the “closed” means.

The fixed-share count nature of CEFs allows investors to clearly track their net asset value (“NAV”) and then buy or sell shares based upon the premium/discount to fair value.

The management teams running CEFs often use leverage within the funds to bolster returns and the distribution yields that they provide.

Leverage is always a risk. But it can come with reward. And in the case of CEFs, that reward is usually a distribution yield in the 7% to 10% range.

Unlike ETFs, which provide dividend yields based upon the dividend paid by their holdings, CEFs have the freedom to return a percentage of their NAV to shareholders as a distribution each year. Distribution policies vary from fund to fund but can be found on their websites/prospectuses.

What this means for investors is that they can select funds with baskets of stocks that they like, such as U.S. large-cap technology or global infrastructure assets, and then collect an abnormally high yield based upon the underlying growth of these holdings.

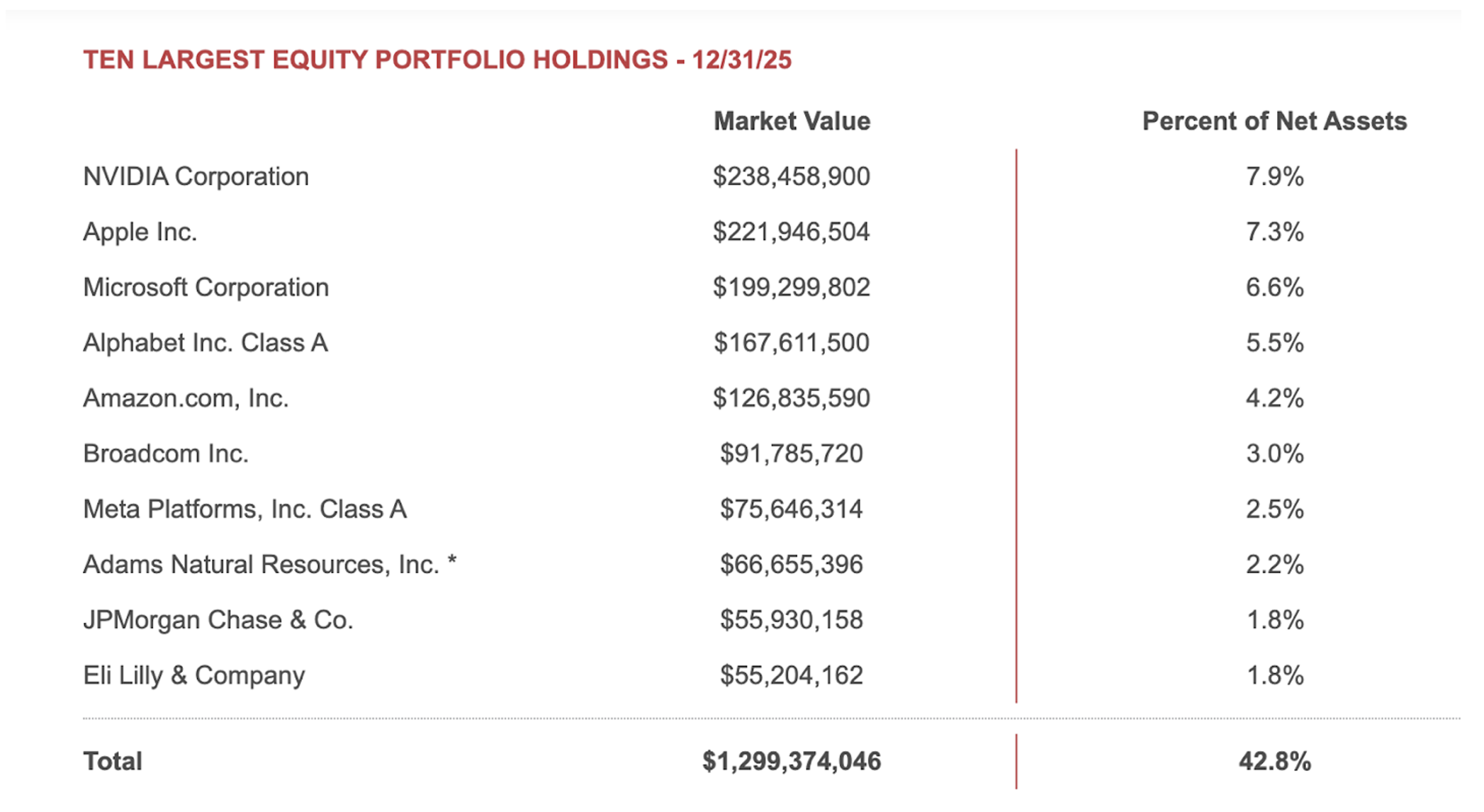

For instance, let’s look at Adams Diversified Equity Fund (ADX). This CEF has been around for 96 years. As you can see below, its top 10 holdings largely mirror the tech-heavy Nasdaq. However, unlike Invesco QQQ Trust (QQQ), which yields only 0.46%, ADX currently provides investors with an 8.16% yield.

Source: ADX Investor Relations

You might think this yield is too good to be true. Oftentimes, when we see funds holding technology, but providing a high yield, what they’re doing is stealing from Peter to pay Paul. Put another way, they’re simply returning investors’ capital back to them in the form of a distribution. This is inefficient from a taxation standpoint and typically serves as a drag on total returns. Yet, that’s not the case with ADX.

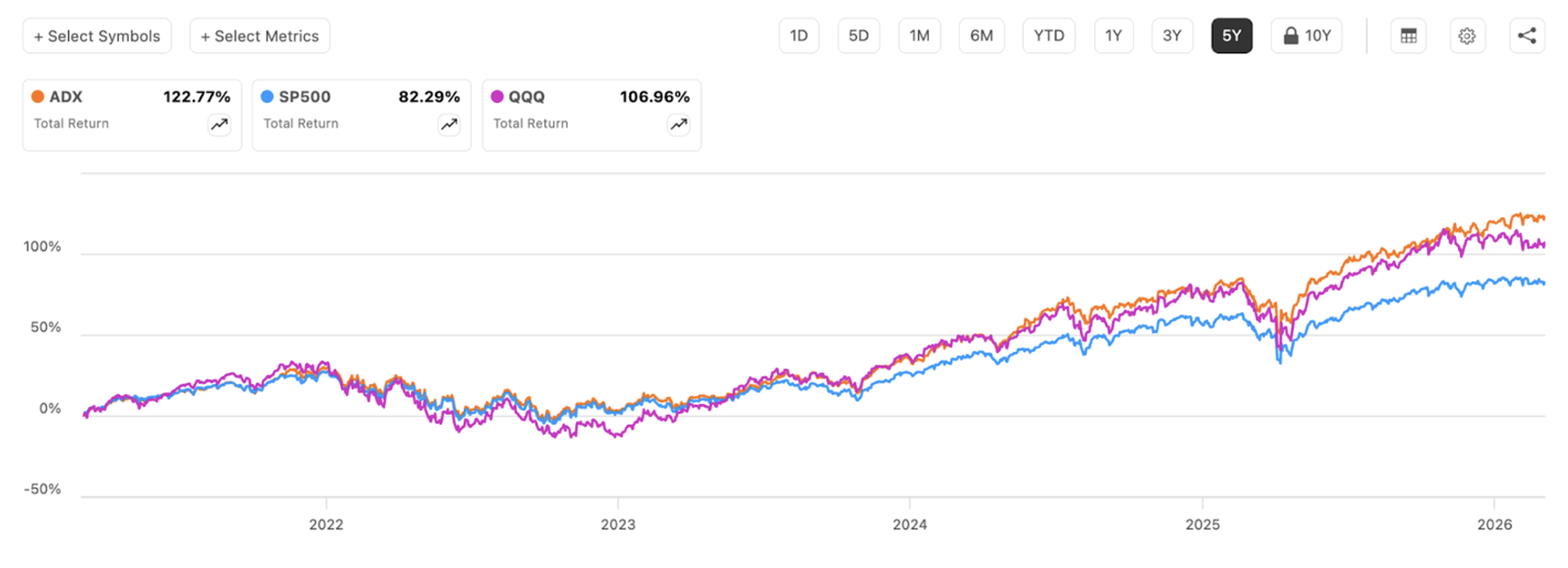

As you can see below, the Adams Diversified Equity Fund has outperformed both the S&P 500 and the Nasdaq Composite Index over the past five years.

Source: Seeking Alpha

This is due to the firm’s top-notch management team and their ability to manage their portfolio in a way that generates NAV growth that outpaces the market, while still returning a generous amount of capital to their shareholders.

As I write, ADX trades at a negative 3.9% discount to its NAV.

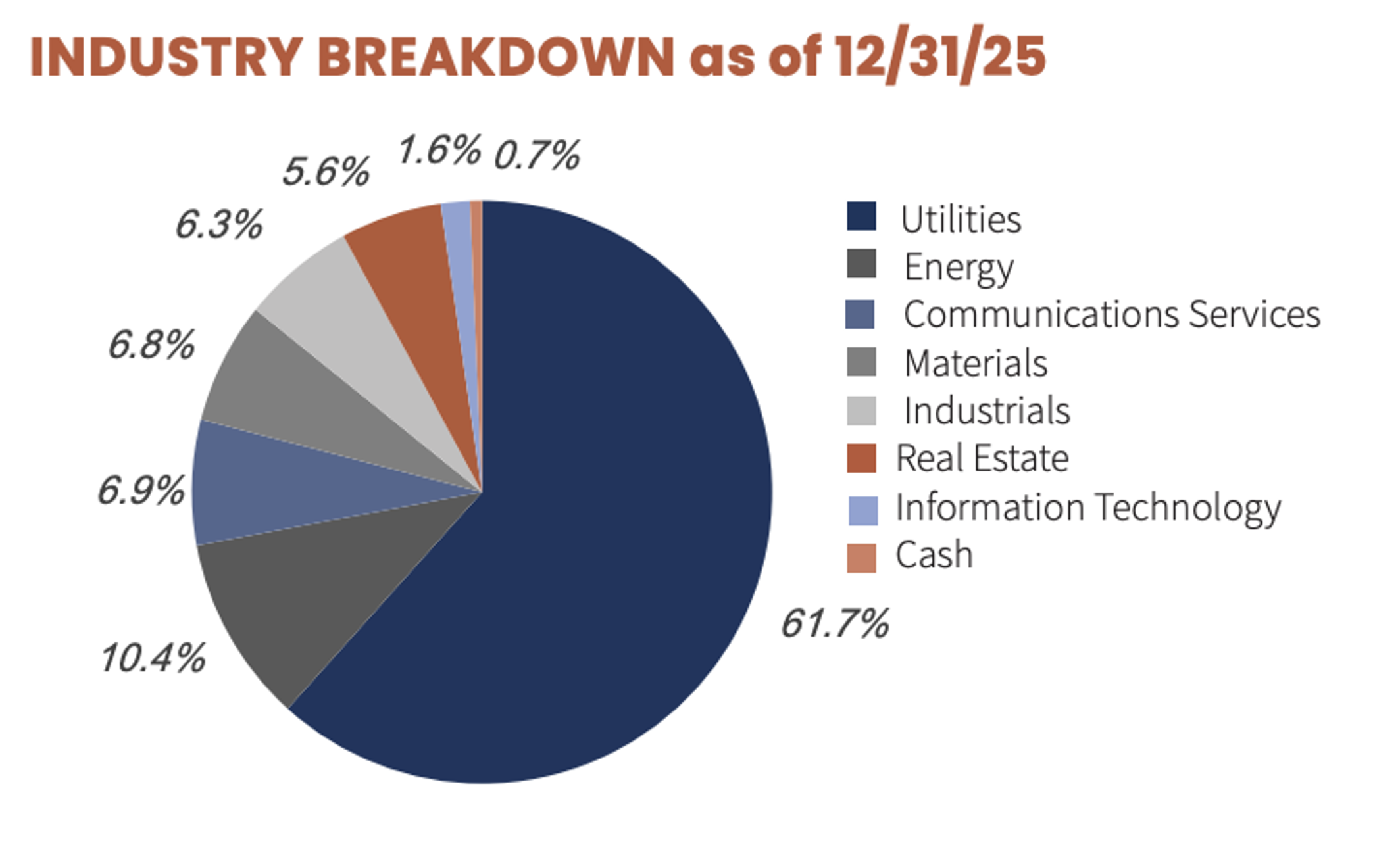

Another example of a high-performing CEF is the Reaves Utility Income Fund (UTG). This fund focuses on companies that own cash-flowing hard assets such as electric utilities, gas/oil pipelines, real estate, data centers, and cell phone towers.

Typically, these types of investments already pay high dividends. But UTG is able to provide exposure to them while bolstering yield with a combination of leverage and NAV distribution policies.

Source: UTG Investor Factsheet

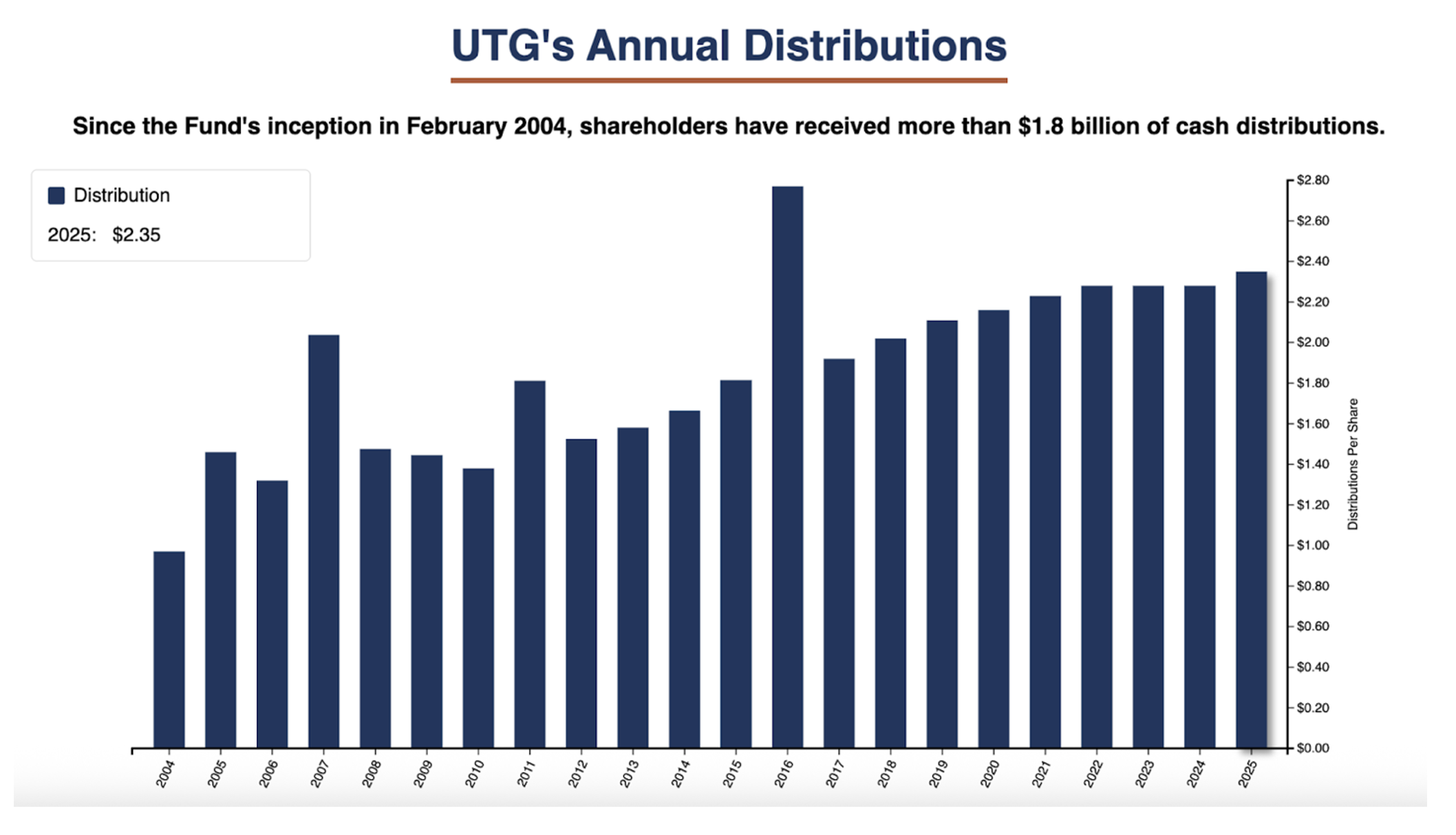

Of course, leverage is always a double-edged sword. But as you can see below, this management team has established a long history of providing reliably growing distributions and a much higher yield than can be found with comparable ETFs.

Source: UTG Website

Currently, UTG offers a 6% yield. That’s more than twice as high as the State Street Utilities Select Sector SPDR Fund (XLU), which currently yields 2.51%.

As I write, UTG trades at a negative 0.82% discount to its NAV.

To be clear, not all CEFs are created equally. Investors must do their due diligence before buying these assets.

So often, the success – or lack thereof – of a CEF comes down to its management team. So, the portfolio managers and investment analysts working for these funds must be vetted. But there are CEFs out there with sound investment strategies that own high-quality assets, have long histories of distributions, and provide investors with outsized yields.

These yields are key to building a bridge to retirement.

They can boost passive income in the present while also protecting (and potentially growing) your principal so that when it’s all said and done, you can also provide financial windfalls to loved ones or organizations that deserve it.

Regards,

Nick Ward

Analyst, Wide Moat Research

Full disclosure: I am a current investor in both closed-end funds mentioned today.

|