I’ve probably annoyed at least a few of you while defending single-family rental (“SFR”) landlords this year.

That’s obviously not my goal. People are frustrated after being priced out of the housing market for six years now.

And they can’t help but notice how institutional investors like massive asset manager Blackstone (BX) – which I wrote about in February – and real estate investment trusts (“REITs”), like Invitation Homes (INVH) and American Homes 4 Rent (AMH), just keep adding to their portfolios.

My purpose today isn’t to talk them up yet again (as I did here, here, and here).

But I do have to review the SFR structure again, nonetheless, to set Millrose Properties (MRP) up.

This new company is a direct product of the evolving expectations and capabilities within the REIT universe – specifically in interacting with the housing market. And it’s one that might sit much better with anti-SFR investors than my previous recommendations.

The Background That Sets Millrose’s Stage

If we lived in a perfect economy, homes would sell as soon as they hit the market. But unfortunately for homebuilders like D.R. Horton (DHI), Lennar (LEN), PulteGroup (PHM), and NVR (NVR), that’s just not the case.

It can be difficult to gauge future housing conditions when it takes up to 30 months to bring a new development to market. In which time, of course, a good economy can go bad.

Fortunately for homebuilders, SFR REITs and like-minded institutional investors have stepped in to save the day over the past decade.

Once mere buyers of pre-owned homes, these landlords branched out into new communities, becoming reliable, large-scale buyers – particularly in Sun Belt markets, where business is booming.

Moreover, many of these buys were pre-planned through strategic partnerships that benefited everyone involved. Homebuilders got “perfect economy” guaranteed sales. The markets stayed more balanced as institutional investors served as essential shock absorbers…

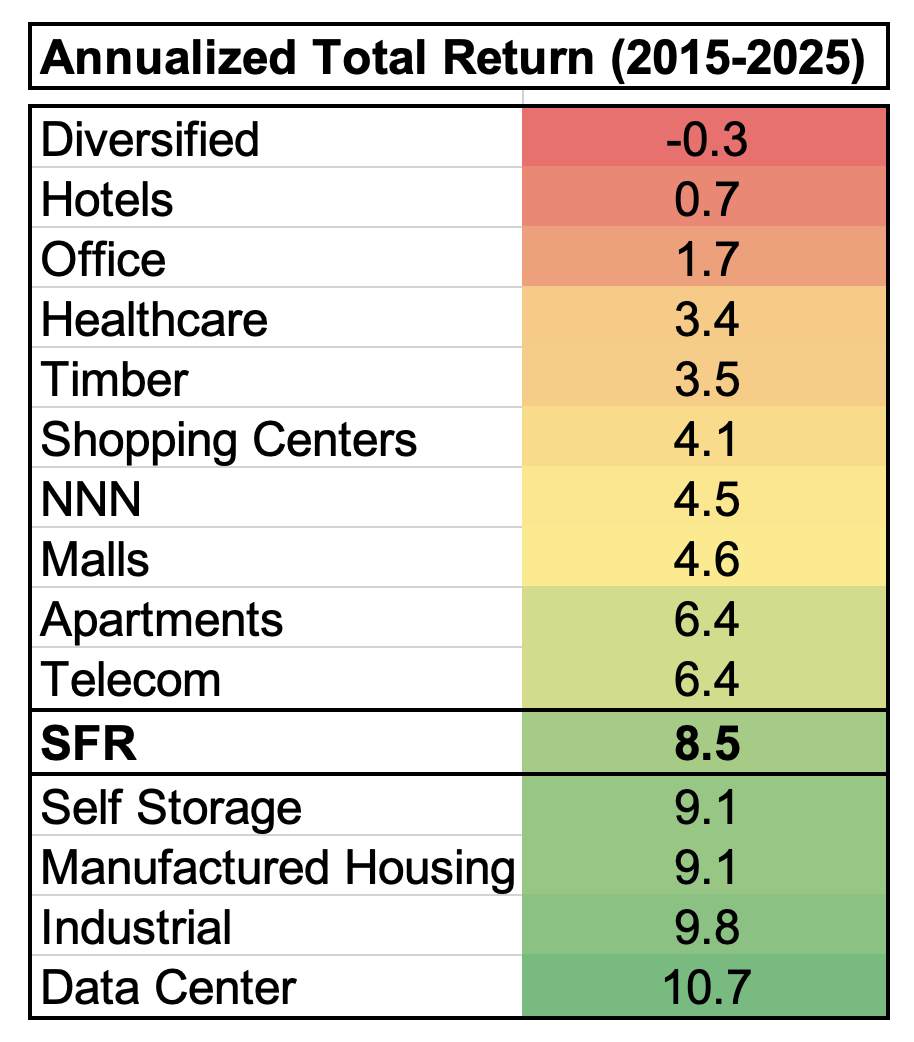

And SFR landlords got top-grade houses to rent out to quality customers, helping them crack the top five REIT subsectors for annualized total returns.

Source: Wide Moat Research / NAREIT

That positive evolution hasn’t stood out to lawmakers in the last year, however. They’ve zeroed in on the idea that institutional investors have run ragged all over the American Dream.

Encouraged by President Donald Trump, proposals are well on their way to increasing oversight of such purchases to severely limit their ability to buy properties.

I still believe these innovative REITs will find a way to succeed, for the record – as I discussed on my YouTube show last week, where I featured AMH and INVH.

However, it’s obvious they’re at greater risk than they have been in quite a while. And it’s that very risk that opened up another creative investment opportunity.

Millrose: A New Kind of REIT Solution

Before a home can be built, developers must first acquire land, entitle it, and develop infrastructure. That’s part of the reason why the process takes so long, tying up significant capital in the process.

So, faced with lagging headwinds and changing legal dynamics, Lennar decided to spin off part of its business into a “first of its kind” homesite option purchase platform called Millrose. That way, it gets to focus on building beautiful homes while its free-standing affiliate can focus on holding land.

And all under a tax-friendly structure, since REITs don’t have to pay taxes on their annual income. This is just one more example of how REITs are evolving into the capital partner space, as I noted on Monday.

Millrose specifically is a mortgage REIT, or mREIT, since it’s built around financing land for homebuilders. But it’s an mREIT with a twist since it also owns physical properties through option agreements with its builder-clients who pay Millrose recurring returns in the process.

Lennar, for instance, pays Millrose an 8.5% annual option fee per property. And it’s seeing strong demand from other homebuilders as well – to the point where it expects to grow invested capital by $2 billion this year even without Lennar’s master program.

With it, that anticipated amount grows to $10.5 billion.

Millrose has a geographically diverse portfolio that spans 30 states and 933 communities, with particular strength in markets such as:

-

Charlotte, North Carolina

-

Columbia, Maryland

-

Charleston, South Carolina

-

My hometown of Greenville, South Carolina.

The REIT already delivered more than 31,000 homesites to builders last year. Moreover, the resulting average home selling price was approximately 20% below the national average for new single-family homes.

So even if we do see a correction in the homebuilding market, Millrose is still well-positioned to thrive.

Millrose’s Beautiful Balance Sheet

Millrose’s balance sheet is in great shape, with total assets of approximately $9.3 billion and total debt of $2.1 billion. That results in a debt-to-capitalization ratio of approximately 26% – much lower than net-lease REITs at 46% or commercial mREITs at 79%.

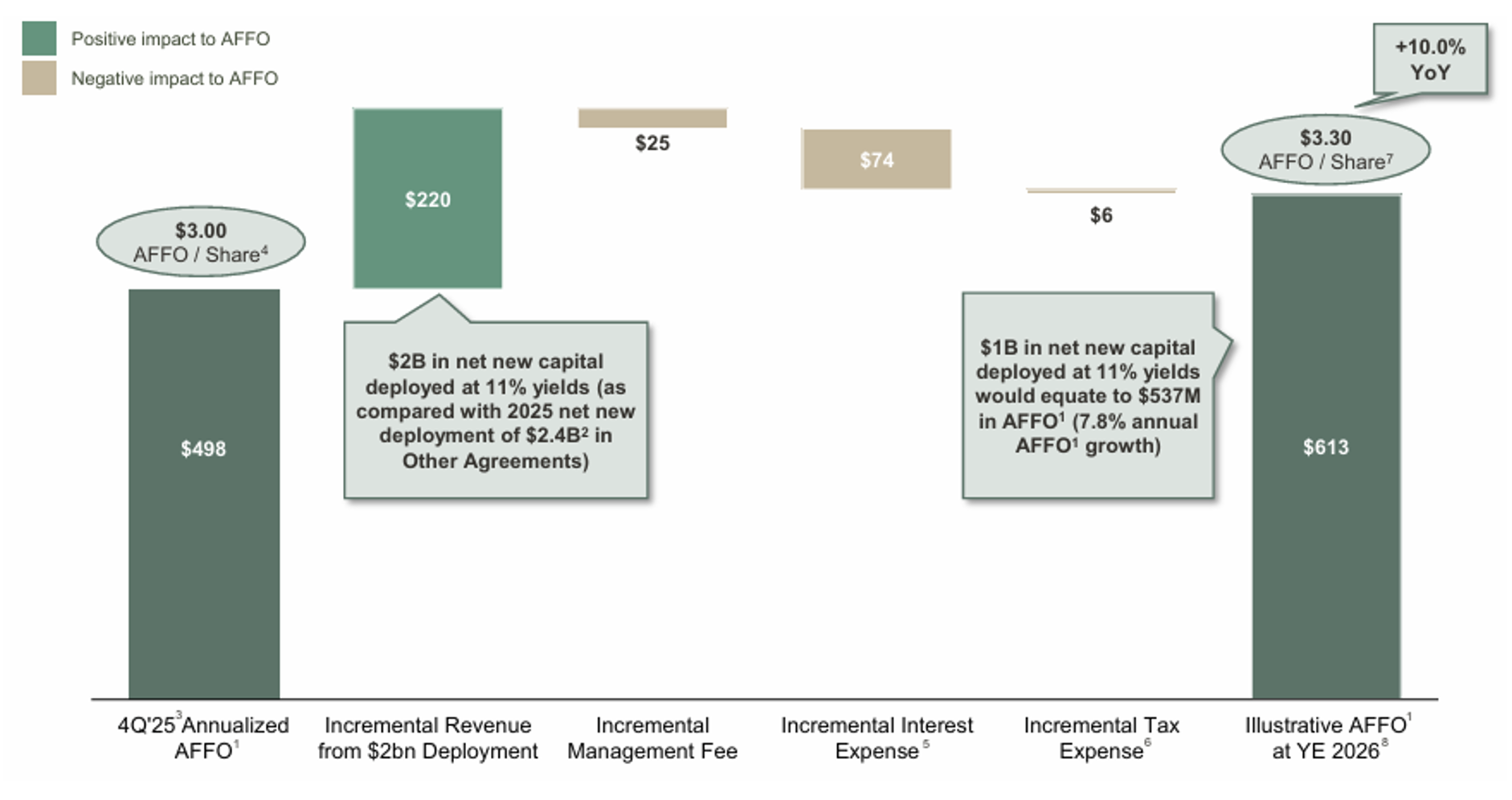

One thing I find especially interesting is that Millrose delivered higher adjusted funds from operations (“AFFO”) across every quarter of 2025. And given its low leverage and contractual income structure, it’s predicting that per-share AFFO will grow by 10% annually over the next two years.

As seen below, deploying $1 billion of net new capital at current yields would drive more than 7% growth in AFFO per share. And executing on $2 billion, as it’s projecting, would imply a growth target of 10%.

Source: Millrose Investor Presentation

Better yet, since Millrose’s earnings stream is paid out to investors in the form of dividends… I suspect its dividend growth could be around 10% as well.

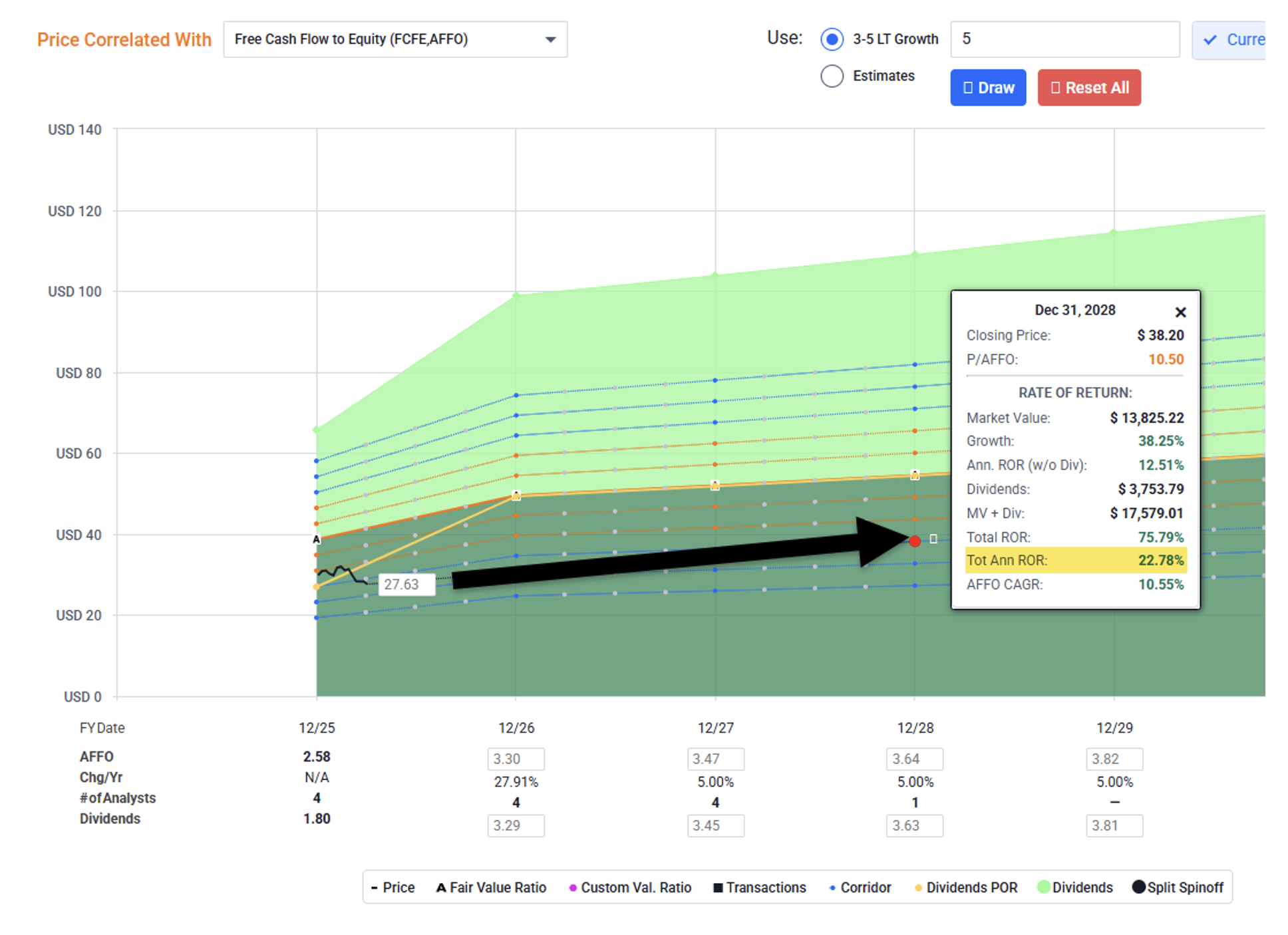

Now, in terms of valuation, shares are trading at roughly 10 times price-to-AFFO estimates. That makes this REIT-dom newbie look like an attractive high-yielder.

As shown below with the FAST Graphs forecasting tool, assuming a 10.6% current dividend yield and 5% growth in 2027 – plus modest price appreciation – we’re looking at a potential annualized return of 22%.

Source: FAST Graphs

So if you’re looking for some housing market love even under these current conditions, Millrose might be right for you. We know that we’ll be adding it regardless to our Wide Moat high-yield shopping list.

This REIT is one of the rare occasions in which you can have your cake (10% dividend yield) and icing (10% growth), which translates into a 20% total return possibility. Who’s ready to dig in?

Regards,

Brad Thomas

Editor, Wide Moat Daily

|